The world of cryptocurrency has evolved far beyond buying, holding, and trading digital assets. For investors looking to make their crypto work for them, crypto lending has emerged as a powerful tool to earn passive income.

But how does crypto lending work, and how much can you realistically earn? Well, this guide breaks it down step by step, offering practical examples, comparisons, and strategies to help you navigate the crypto lending landscape.

- Introduction to crypto lending

- How crypto lending works

- Types of crypto lending platforms

- Borrower vs. lender perspectives

- Earnings from crypto lending

- Risks of crypto lending

- Crypto lending vs. other crypto income methods

- Choosing the right crypto lending platform

- Best practices for safe crypto lending

- Conclusion

- Frequently asked questions (FAQs)

Introduction to crypto lending

Crypto lending is the process of lending your cryptocurrency to borrowers in exchange for interest payments. Much like a traditional bank lends money, crypto lending allows investors to generate returns without selling their digital assets.

Unlike conventional banking, which relies on fiat currency and centralized institutions, crypto lending operates on centralized (CeFi) and decentralized (DeFi) platforms. Borrowers can access liquidity while lenders earn interest — often at rates higher than typical savings accounts or bonds.

Why crypto lending has grown in popularity:

- It transforms idle crypto assets into a source of passive income.

- Borrowers can access liquidity without selling their holdings or having to buy crypto.

- Platforms make it easy to lend and borrow globally, often without credit checks.

How crypto lending works

The process is simple in theory, but involves several important steps:

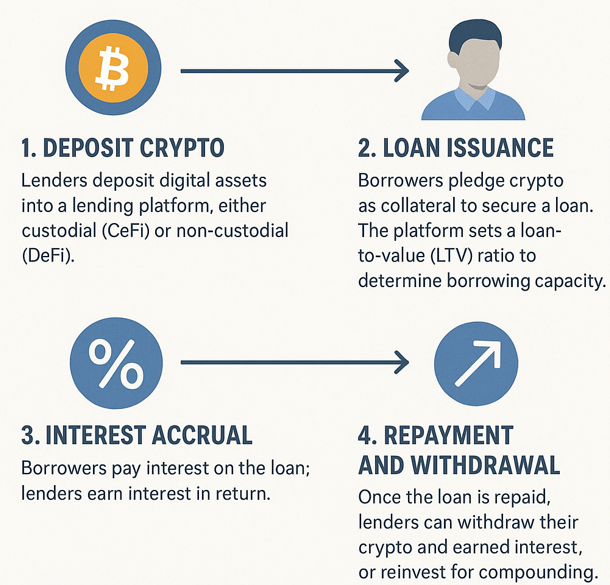

The step-by-step process of crypto lending

- Lender deposits crypto into a lending platform.

- A borrower takes a loan from the lending platform against collateral, which is usually another type of crypto that they have deposited in the lending platform. Crypto loans are mostly overcollateralized.

- The loan taken by the borrower accrues interest.

- The borrower repays the loan plus accrued interest.

- The lender withdraws the deposited crypto plus interest or reinvests it for compounding.

Example:

- You deposit 10 ETH into a lending platform.

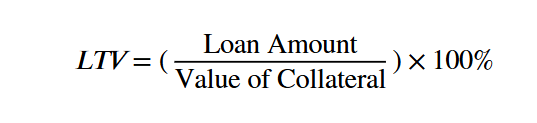

- A borrower takes an ETH loan using placing some other crypto as collateral with a loan-to-value (LTV) of 50%.

- If the borrower’s collateral is, for example, worth $20,000, the borrower can access $10,000 worth of an ETH loan.

Here is how the LTV works in crypto loans:

- Let us say over a 6-month loan term, the borrower pays 8% annual interest. So, you earn $400 in interest while retaining your 10 ETH.

Overcollateralization

Most crypto loans are overcollateralized, meaning the collateral exceeds the loan amount to protect lenders from price drops. Typical overcollateralization ratios are 150–300%. For example, to borrow $1,000, a borrower may need to pledge $2,000–$3,000 worth of crypto.

Types of crypto lending platforms

Centralized Finance (CeFi)

- Managed by a central company that acts as a custodian.

- Integrates regulatory compliance, such as KYC and AML.

- Offers security features like cold storage and sometimes insurance.

Examples include: Binance, Nexo, and CoinLoan.

Decentralized Finance (DeFi)

- Operates using smart contracts on blockchain networks.

- No central authority; peer-to-peer transactions.

- Interest rates fluctuate based on the liquidity pool supply and demand

Examples include: Aave and Compound.

| Feature | CeFi | DeFi |

| Custody | Platform holds assets | User retains control via smart contracts |

| Regulation | Compliant (KYC/AML) | Often unregulated |

| Interest Rates | Stable | Variable, depends on supply/demand |

| Accessibility | May require geo-restrictions | Global, pseudonymous |

| Security Risks | Hacks, mismanagement | Smart contract vulnerabilities |

Borrower vs. lender perspectives

For Borrowers:

- Access liquidity without selling crypto.

- Pay interest, which may be lower than unsecured loans.

- Risk of collateral liquidation if crypto prices drop.

For Lenders:

- Earn passive income via interest payments.

- Retain ownership of assets (cannot trade while collateralized).

- Risks include borrower default and platform failure.

Earnings from crypto lending

Interest rates vary depending on the platform and asset type.

| Asset Type | Typical Interest Rate (APY) |

| Bitcoin (BTC) | 3–7% |

| Ethereum (ETH) | 3–7% |

| Stablecoins (USDC, USDT) | 10–18% |

| High-risk altcoins | Up to 20% |

Example:

- Lending 5 ETH at 5% APY for one year earns: 5 × $2,000 × 5% = $500

- Lending $10,000 in USDC at 12% APY earns: $10,000 × 12% = $1,200

Factors affecting returns:

- Platform policies and fees

- Type of cryptocurrency

- Market demand and liquidity

- Loan duration and LTV ratio

Risks of crypto lending

Crypto lending can be lucrative, but comes with unique risks:

- Market Volatility: Collateral value may fall, triggering margin calls or liquidation.

- Borrower Default: Collateral may not fully cover the loan if markets crash.

- Platform Security: CeFi platforms can be hacked; DeFi smart contracts may have bugs.

- Regulatory Uncertainty: Changing laws can impact platform operations and accessibility.

Example of liquidation risk:

- Borrower pledges $3,000 in ETH to secure a $1,000 loan.

- ETH price drops 50%, collateral now worth $1,500.

- The platform may automatically liquidate part of the collateral to cover the loan.

Crypto lending vs. other crypto income methods

| Feature | Lending | Staking | Holding |

| Income Source | Borrower interest | Blockchain rewards | None |

| Liquidity | Medium–high | Low (locked for staking) | High |

| Risk | Borrower default, platform security | Network failure, asset drop | Market volatility |

| Asset Control | Retained, limited use | Locked | Full |

Key takeaways:

- Lending provides passive income while maintaining asset ownership.

- Staking supports blockchain networks and generates rewards but often locks your assets.

- Holding is safe but unproductive; crypto does not earn passive income on its own.

Choosing the right crypto lending platform

Factors to consider:

- Interest rates: Compare rates for different crypto assets.

- Fees: Origination, withdrawal, liquidation, and platform fees.

- Loan terms: Duration, fixed vs. variable interest, minimum deposit.

- Collateral requirements: LTV ratios vary by platform.

- Security & insurance: Cold storage, audits, and insurance coverage.

- Regulatory compliance: KYC/AML policies and geo-restrictions.

Example comparison:

| Platform | Type | Supported Assets | Typical Interest | Security Features |

| Binance | CeFi | BTC, ETH, 65+ cryptos | 3–10% | Cold storage, KYC, insurance |

| CoinLoan | CeFi | BTC, ETH, USDT, fiat | 5–12% | Zero incidents in 5 years, multiple loans allowed |

| Aave | DeFi | ETH, DAI, USDC | Variable | Smart contracts, transparent blockchain ledger |

| Compound | DeFi | ETH, USDC, DAI | Variable | Non-custodial, automated contracts |

Best practices for safe crypto lending

- Diversify Platforms and Assets: Reduces exposure if one platform fails.

- Secure Your Funds: Use cold storage or non-custodial wallets.

- Review LTV Ratios & Collateral: Lower ratios reduce liquidation risk.

- Understand Fees & Terms: Avoid hidden costs and platform traps.

- Monitor Markets: Be prepared for volatility and margin calls.

Conclusion

Crypto lending offers a dynamic way to generate passive income, combining the flexibility of digital assets with the mechanics of traditional lending. By understanding the process, selecting the right platform, and managing risks carefully, both borrowers and lenders can benefit from this growing sector.

Key takeaways:

- Crypto lending allows you to earn interest while retaining ownership of your assets.

- Stablecoins offer predictable returns; volatile cryptos can offer higher yields but with higher risk.

- Diversifying platforms and monitoring LTV ratios protects against market volatility.

- CeFi platforms provide security and regulation, while DeFi platforms offer automation and decentralization.

By making informed decisions and practicing risk management, crypto lending can become a profitable and strategic addition to your crypto portfolio.

Frequently asked questions (FAQs)

What is crypto lending?

Crypto lending is the process of lending your digital assets to borrowers in exchange for interest payments.

How much can I earn from lending crypto?

Earnings vary by asset and platform, with typical APYs ranging from 3% for Bitcoin to 18% for stablecoins.

Is crypto lending safe?

Crypto lending carries risks like market volatility, borrower default, and platform security breaches.

What is the difference between CeFi and DeFi lending platforms?

CeFi platforms are centralized and regulated, while DeFi platforms operate on smart contracts without intermediaries and offer variable rates.